Click on The Appropriate Section Click on The Appropriate Section

NOVEMBER 25th 2009 IS

A LANDMARK DAY IN BANKING HISTORY. FOR THE

BANKS HAVE BASICALLY WON A BATTLE BUT IN THE

PROCESS HAVE LOST THE WAR

Yes the OFT

have lost their case against the Banks on

a technicality but in the 46 page summing

up the Supreme Court made it clear that

the underlying reasons of the OFT claim

were right and that the banks have not

just been overcharging but by their own

devious actions have been creating

unauthorised overdrafts so as to then take

massive disproportionate charges. This we

realised some time ago especially where

the banks have tried to take a charge of

up to £8 a day on overdrafts of a few

pence. Their little game is to allow an

unauthorised overdraft of a few £'s so

that they can claim their large daily rate

and then bounce any further payments. The

question is why did they allow the

original unauthorised overdraft in the

first place. In most cases the customer

didn't request the overdraft- therefore

the debt is the fault of the bank and the

Customer should NOT pay such charges.

To the OFT, the Supreme Court hinted that

it might want to look at a different

section of the law. Instead of regulation

six, it should look to regulation five. By

not allowing the customers to have a say

in whether the bank should accept

transactions that take them beyond their

unauthorised overdraft limit, for example,

the banks could be said to be in breach of

this regulation. Therefore we shall take

every case we are dealing with to the

Courts under section 5, as we have been

doing for some years now.

We specialize in challenging

Banks & Credit Card Companies in regards

their charges on credit cards and charges for bouncing cheques and

Direct Debits. We also act for people who are

being persued for debts & advise them how to

defend against those debts and the charges that

are being included in them. In most cases

these charges are disproportionately high and it

is likely that these Companies are conducting

unfair terms under CONSUMER

CONTRACT REGULATIONS 1999 . Further in many cases they

have been taking insurance premiums to cover debts

if the creditor loses his/her job, but still chase

the creditor when they may have collected an

insurance payout.

We name & shame these

financial institutions who are ripping off their

customers and direct clients to the appropriate

authorities to report them to. In recent months

these actions have gathered pace & the banks

are trying more unfair methods of fighting back

like closing accounts. We can assist you by

further naming & shaming the individuals in

the banks playing such games. Remember they only

got big by servicing the public & if they

abuse the public then they can also meet the

same people on the way down. We have had

questions asked in Parliament and will continue

to fight for the Consumer. We have now added a

list of the leading CEOs in the UK for YOU to

contact direct so avoiding call centres etc

BANK

& CREDIT CARD CHARGES

|

It

really

annoys us when banks and other

financial firms penalise customers

so heavily for their mistakes.

However, when the boot’s on the

other foot, these companies are

quick to deny responsibility and

routinely refuse to pay out

compensation when they mess

up.Therefore, if you’ve got a

grievance, then don’t get mad, get

even. Here are five ways to fight

back against bullying banks:

1. Recover

unauthorised overdraft charges

If

you go overdrawn without

permission, exceed your overdraft

limit, or ‘bounce’ payments from

your current account, then your

bank will punish you for your

mistake. You can expect to pay up

to £40 per slip-up, even if your

unauthorised borrowing is just a

few pounds. However,

the

Office of Fair Trading (OFT)

believes that these punitive

charges are unfair, so it has

taken legal action against eight

banks and building societies.This

case is being heard now.

However

the

Staute of Limitations Act 1980

in English law means that

you can go back six years when

attempting to reclaim these

charges. So, if you’ve been fined

for unauthorised borrowing at any

point since late July 2002, submit

a claim now in writing. Then, when

the OFT finally wins its case,

you’ll already be in the queue for

compensation.

2. Claim back

credit-card fines

Credit

card providers make billions

of pounds every year from

people just like you. They

attach excessive charges at

every available opportunity

and it's not fair. They

could owe you thousands.

Until two years ago, most

credit-card issuers would charge

fines of £20 to £30 for bounced,

late or missed payments, or for

exceeding your credit limit.

However, in April 2006, the OFT

decided that these penalty charges

were unfair. In response to this

ruling, card issuers reduced their

charges to no more than £12 a

time.

Again, if

you’ve been fined by your

credit-card company at any point

in the past six years, then apply

for a refund. Don’t be fobbed off

with excuses, as many card issuers

falsely claim that these

refunds are, like bank-charge

claims, on hold for the duration

of the above court case. Also,

demand full repayment of each fine

-- don’t allow your card issuer to

pay only the difference between

your fine and the ‘fair’ (!) fee

of £12.

|

3. Recoup

mortgage exit arrangement fees

Mortgage

lenders

have also been guilty of

charging massive "exit" fees

on mortgages. If

you have been charged a mortgage

exit arrangement fee greater

than that stipulated in your

contract, then demand a refund

from your mortgage lender. This

massive ‘fee inflation’ is

unfair and, in January 2007, the

Financial Services Authority

(FSA) agreed.

4. Demand

mis-selling compensation

Over the

years we have witnessed massive

mis-selling in the Financial

Services Industry. Our battles

date back to the 1960's and 1970's

when the large insurance companies

went to war with us for giving our

client's discounts on financial

purchases. To-day the authorities

recommend it. We can recall

regulatory failures, mis-selling

problems, FSA fines and

compensation payouts to the public

regarding (in alphabetical order):

- business bank accounts;

- Equitable Life;

- extended warranties;

- free-standing additional

voluntary contributions (extra

pensions);

- guaranteed equity bonds;

- hamper firm Farepak;

- high-income ‘precipice’

bonds;

- home-income plans

(investment mortgages in the

Eighties and Nineties);

- Nation Life (The William

Stern Scandal)

- maximum investment plans;

- mortgage endowments;

- payment protection

insurance;

- personal pensions;

- secured loans (second

mortgages);

- split-capital investment

trusts; and

- store cards.

- Theft of Pension

Dividends in 1997 by Gordon

Brown in breach of pension

contracts.

There

are seventeen scandals in the above

list, but perhaps the most

significant is the widespread

mis-selling of mortgage endowment

policies. Indeed, the possible

shortfall from these failing

part-insurance/part-investment

policies could exceed £50 billion.

This happened because the "terminal

bonus", which had formerly been

given was disapated by companies

purchasing "second hand

policies". |

In

the early nineties we witnessed an

arguement between the principals

of Insurance Companies & the

2nd hand purchasers. Those

Principals are criminally guilty

of allowing past performance to be

shown when THEY KNEW the figures

could not be reproduced.

5. Don’t forget

to charge for your time

Remember

that

you should always insist

that you also be compensated for

inconvenience, distress and time

wasted. So, if your bank charges

you for a computer-generated

letter, return the favour by

charging for the above. If

you are taking time off your work

to spend hours listening to music

on the telephone charge them at an

hourly rate!

6 What

Should You Do Now?

If you have

already made a complaint

- it is likely that your

claim for bank charge refund

will be frozen pending the

outcome of the test

case. If an offer has

been made and you have

accepted that offer, the

bank would be bound to

honour the agreement under

the normal rules of

contract.

If you have

already taken Court Action

- there likely to be a

direction from the Courts

that all actions will also

be frozen. This is

usual in test cases as this

will save court time, costs,

duplication of work and a

prevention of conflicting

court judgements.

Cases will then be reviewed

once a final decision from

the test cases are handed

down.

If

you have not made a

complaint to date

- it is our advice that you

should contact us and make a

formal claim now. If

the test claims win at

court, as you have

registered your claim, it

will help speed up the claim

process. In simple

terms you are more likely to

be paid out earlier.

We cannot make any

guarantees but in our

experience in test cases

this often happens.

Groups of claimants who have

been waiting longer for the

test case to conclude would

normally be those who are

paid out first.

We would imagine that if the

test case is successful

there would be a mass of

people putting in claims

which would result in severe

delays.

You should register with

us now by

contacting us on 0870 794

2180 or

Contact

us by clicking here

and we will contest the

charges.

(UK Only)

|

Update February 26th 2009

Eight

banks have lost an appeal aimed at

stopping the investigation

into overdraft charges, so the legal

battle goes on.

We have

cheery news for fed-up banking customers:

the banks have lost their latest attempt to

halt the Office of Fair Trading (OFT)

investigation into unfair overdraft fees

charged by current

accounts.

The OFT wins round one

Eight

banks -- Barclays, Clydesdale, HBOS, HSBC,

Lloyds TSB, RBS and Nationwide BS -- argued

that the OFT did not have the authority to

investigate whether their charges for

unauthorised overdrafts were unfair and,

therefore, unenforceable. The Court of

Appeal disagreed and backed the OFT.

THE

LEGAL POSITION AS OF OCTOBER 2008

For some time now

there have been a series of hearings as

the Office of Fair Trading has been

challenging the Banks on their charges.

The current position for you in four

simple bullet points:

- The High Court has ruled that the

OFT can assess whether charges are

unfair and take action against the

banks, but the banks have appealed this

decision and we await the appeal

hearing. Whether the OFT chooses to take

action against the banks remains to be

seen.

- The banks have almost totally

closed one of the arguments - that the

charges are unlawful penalties under

common law. The charges could still be

unlawful penalties under totally

different law: the UTCCR.

- The FSA waiver remains

in place, meaning people can’t at the

moment reclaim charges but the banks can

continue to charge them. Wealthier

people continue to pay nothing for their

current accounts.

- Only when all this is over will

we know whether we can reclaim charges,

and whether the banks will continue to

charge us or scrap free banking.

-

Avoid

this devious credit card sting!

Donna

Werbner Published

in

Credit

cards on 16 March 2009

-

|

Using

this little-known trick,

companies can take automatic

payments from your credit

card - even after you've

closed it down!

Imagine this. You pay

off your credit

card, close down

the account and cut up the

card. All is settled until

months later, out of the

blue, you get a statement

from the credit card

provider, demanding payment

for a new transaction on the

card. It's for a 'recurring

payment' - and it's one of

the slimiest credit card

stings ever hidden in the

small print.

How recurring

payments work

On the surface, a

recurring payment works in

exactly the same way as a

direct debit. You authorise

a company to take regular

payments - say, for an

annual subscription or

service - from your credit

card. Simple, easy,

convenient... until you want

to cancel it.

Unlike a direct debit,

a recurring payment does not

automatically cease to exist

when you close your account

down. You cannot even cancel

it by notifying your credit

card provider that you want

it to stop. The only way to

cancel a recurring payment

is to ask the original

merchant you set it up with

to stop taking the payments.

A dangerous

system

As if that wasn't

enough, there are two big

dangers associated with this

method of payment:

You and you alone are

responsible for keeping a

record of all the recurring

payments you have set up on

your card. The credit card

provider will not keep track

of them. And if you don't know

which companies are authorised

to take recurring payments

from your card, then you will

not be able to cancel the

payments.

If you cancel the account and

then, say, move house, your

statement will go to your old

address. So you will have no

way of knowing that a new

payment has been taken from

your card, and that you need

to pay it off. |

This

could lead to a black mark

being placed on your credit

record, which could cause

you serious

problems if you try

to take out a new card or

borrow a mortgage in the

future.

So

if you're ever faced with

the option of making a

regular payment by credit

card or direct debit, my

advice would be to choose

the direct debit route every

time.

Too

late

If

this advice comes a little

too late for you - -

then what can you do about

it?

Neil

wrote in to lovemoney.com

because, six months after

cancelling an MBNA credit

card, he received a

statement stating that more

than £90 had been paid from

the card to a car breakdown

company. This was for cover

he no longer needed or

wanted.

What

to

do

What

should you do if you find

yourself in this situation?

1.

Dispute

the payment with the

company that took it.

Believe

it or not, you are much more

likely to get a refund this

way than arguing with the

credit card company that you

closed the account or

weren't aware that the

payment would recur. Here's

how to argue your case:

- A reputable company

will send you a letter

warning you that your

subscription is up for

renewal, and that payment

will be taken on a

particular date. If you

didn't receive this

letter, you have a case

for disputing the payment.

|

Depending

on what you have bought, you

should have a cooling off

period of at least seven days,

where you can cancel the

policy or return the goods.

Contact Consumer

Direct to double-check

your rights, if you find this

cooling off period is

disputed. You may even have

longer than seven days.

Finally,

try explaining your situation

calmly and reasonably. For

example, Neil, our 66-year-old

reader, no longer drives a car

and therefore has no need for

car breakdown cover. Clearly,

he would not have renewed this

cover voluntarily. Most

reputable companies will take

a reasonable attitude when

there is a clear case for a

refund like this. If they

don't, you could try reporting

them to a relevant regulator

or trade body.

2.

Dispute

the payment with the credit

card provider.

If

you fail to get a refund

from the company that took

the payment, it's still

worth at least trying to get

a refund from the credit

card provider - although it

may be difficult.

If you have cancelled

your card, you could argue

that you hadn't realised that

the payment would be taken.

This is especially true if it

is obvious, as in Neil's case,

that you would never have

knowingly renewed the

subscription or service.

Alternatively,

do

bear in mind you have Section

75

Protection for payments

over £100. So if the product

cost more than £100 and was

misrepresented to you in any

way, you could dispute the

payment on these grounds.

Using

these arguments, I am

pleased to say Neil

successfully managed to get

his payment refunded - but

only after Citizens Advice

got involved.

Many

of you with recurring

payments on your cards may

not be so lucky. So watch

out for this nasty little credit

card sting - and

stick to direct debits

whenever you can!

|

Using this

little-known trick, companies can take

automatic payments from your credit card

- even after you've closed it down!

Imagine this. You pay off your credit card,

close down the account and cut up the

card. All is settled until months later,

out of the blue, you get a statement

from the credit card provider, demanding

payment for a new transaction on the

card. It's for a 'recurring payment' -

and it's one of the slimiest credit card

stings ever hidden in the small print.

How recurring payments work

On the surface, a recurring payment

works in exactly the same way as a

direct debit. You authorise a company to

take regular payments - say, for an

annual subscription or service - from

your credit card. Simple, easy,

convenient... until you want to cancel

it.

Unlike a direct debit, a recurring

payment does not automatically cease to

exist when you close your account down.

You cannot even cancel it by notifying

your credit card provider that you want

it to stop. The only way to cancel a

recurring payment is to ask the original

merchant you set it up with to stop

taking the payments.

A dangerous system

As if that wasn't enough, there are two

big dangers associated with this method

of payment:

- You and you alone are responsible for

keeping a record of all the recurring

payments you have set up on your card. The

credit card provider will not keep track

of them. And if you don't know which

companies are authorised to take recurring

payments from your card, then you will not

be able to cancel the payments.

- If you cancel the account and then, say,

move house, your statement will go to your

old address. So you will have no way of

knowing that a new payment has been taken

from your card, and that you need to pay

it off. This could lead to a black mark

being placed on your credit record, which

could cause you serious problems

if you try to take out a new card or

borrow a mortgage in the future.

So if you're

ever faced with the option of making a

regular payment by credit card or direct

debit, my advice would be to choose the

direct debit route every time.

Too late

If this advice

comes a little too late for you - as it did

for one lovemoney.com reader, Neil D. - then

what can you do about it?

Neil wrote in to

lovemoney.com because, six months after

cancelling an MBNA credit card, he received

a statement stating that more than £90 had

been paid from the card to a car breakdown

company. This was for cover he no longer

needed or wanted.

What to do

What should you

do if you find yourself in this situation?

1. Dispute the

payment with the company that took it.

Believe it or

not, you are much more likely to get a

refund this way than arguing with the credit

card company that you closed the account or

weren't aware that the payment would recur.

Here's how to argue your case:

- A reputable company will send you a

letter warning you that your subscription

is up for renewal, and that payment will

be taken on a particular date. If you

didn't receive this letter, you have a

case for disputing the payment.

- Depending on what you have bought, you

should have a cooling off period of at

least seven days, where you can cancel the

policy or return the goods. Contact Consumer

Direct to double-check your rights,

if you find this cooling off period is

disputed. You may even have longer than

seven days.

- Finally, try explaining your situation

calmly and reasonably. For example, Neil,

our 66-year-old reader, no longer drives a

car and therefore has no need for car

breakdown cover. Clearly, he would not

have renewed this cover voluntarily. Most

reputable companies will take a reasonable

attitude when there is a clear case for a

refund like this. If they don't, you could

try reporting them to a relevant regulator

or trade body.

2.

Dispute the payment with the credit

card provider.

If you fail to

get a refund from the company that took the

payment, it's still worth at least trying to

get a refund from the credit card provider -

although it may be difficult.

- If you have cancelled your card, you

could argue that you hadn't realised that

the payment would be taken. This is

especially true if it is obvious, as in

Neil's case, that you would never have

knowingly renewed the subscription or

service.

- Alternatively, do bear in mind you have

Section

75

Protection for payments over £100.

So if the product cost more than £100 and

was misrepresented to you in any way, you

could dispute the payment on these

grounds.

Using these

arguments, I am pleased to say Neil

successfully managed to get his payment

refunded - but only after Citizens Advice

got involved.

Many of you with

recurring payments on your cards may not be

so lucky. So watch out for this nasty little

credit

card sting - and stick to direct

debits whenever you can!

OUTSOURCING IS A DEVASTATING CAUSE OF RECESSION

IN BRITAIN OUTSOURCING IS A DEVASTATING CAUSE OF RECESSION

IN BRITAIN

Recently

Birmingham City Council announced

that they were going to outsource

to India. Are these idiots really

serious? Instead of promoting

local jobs they are depriving

Birmingham of money. Firstly those

being made redundant go on

Jobseekers allowance and maybe

Housing Benefits and Council Tax

Benefits. Then the local shops and

services lose out as there is less

spending power. All round they

create more recession. This has

got to stop- we suggest that where

British Companies servicing

British people in Britain

outsource outside Europe then the

fees paid for that outsourcing

should be exempt from being

accepted as a trading cost and

disallowed to be shown as such in

their accounts. If you know of

companies doing this let us know

and we shall shame them and others

can avoid using them. Recently

Birmingham City Council announced

that they were going to outsource

to India. Are these idiots really

serious? Instead of promoting

local jobs they are depriving

Birmingham of money. Firstly those

being made redundant go on

Jobseekers allowance and maybe

Housing Benefits and Council Tax

Benefits. Then the local shops and

services lose out as there is less

spending power. All round they

create more recession. This has

got to stop- we suggest that where

British Companies servicing

British people in Britain

outsource outside Europe then the

fees paid for that outsourcing

should be exempt from being

accepted as a trading cost and

disallowed to be shown as such in

their accounts. If you know of

companies doing this let us know

and we shall shame them and others

can avoid using them.

In the meantime your editor

has been receiving 3 to 4 calls a

day on his Orange nobile phone

from a number shown as 0845 450

3102. It appears to be from

Gajwel, Sangareddy, India.

So far they have called 28 times

in a week!. As a dialling machine

is calling I just hear

silemce. They can't be

blocked by TPS because they are

abroad. Even if they talked they

would not be dealt with for

reasons stated above. Orange &

EE have been informed and Orange

subscribers are being

targeted. Mr Osborne please

tax these activities! Here

are some organisations that use

overseas call centres:

BEWARE

THE CHEQUE SCAM OR TIT FOR TAT

by our in-house would-be

sucker

|

| Every so often some

idiot trickster tries to con us on

the internet. This one came through

our Skype connection. Now we

regularly get young ladies from

Ghana or other West African

Countries trying to "chat". After a

few minutes chatting they try to get

us to send money to them. A polite

No usually ends this. But in the

last month one of our older

directors had a so-called young 27

year old "lady" from Gauteng , South

Africa . She sent an email with her

pictures as shown above. One showing

her breast.She claimed that she was

in the Media Pr business and worked

in the field of beauty products. She

also said that she was hoping to

visit England on behalf of her

company, for whom she had worked for

6 months, within the near

future, if selected. Well the next

week she went for an interview and ,

lo & behold, she got picked. On

the

day of selection she contacted our

would be sucker and told him the

good news. |

She would be

coming a week later. But there was

one problem. She had to have money

sent to England by her Company,

whose headquarters were in Germany.

Could our would-be sucker receive it

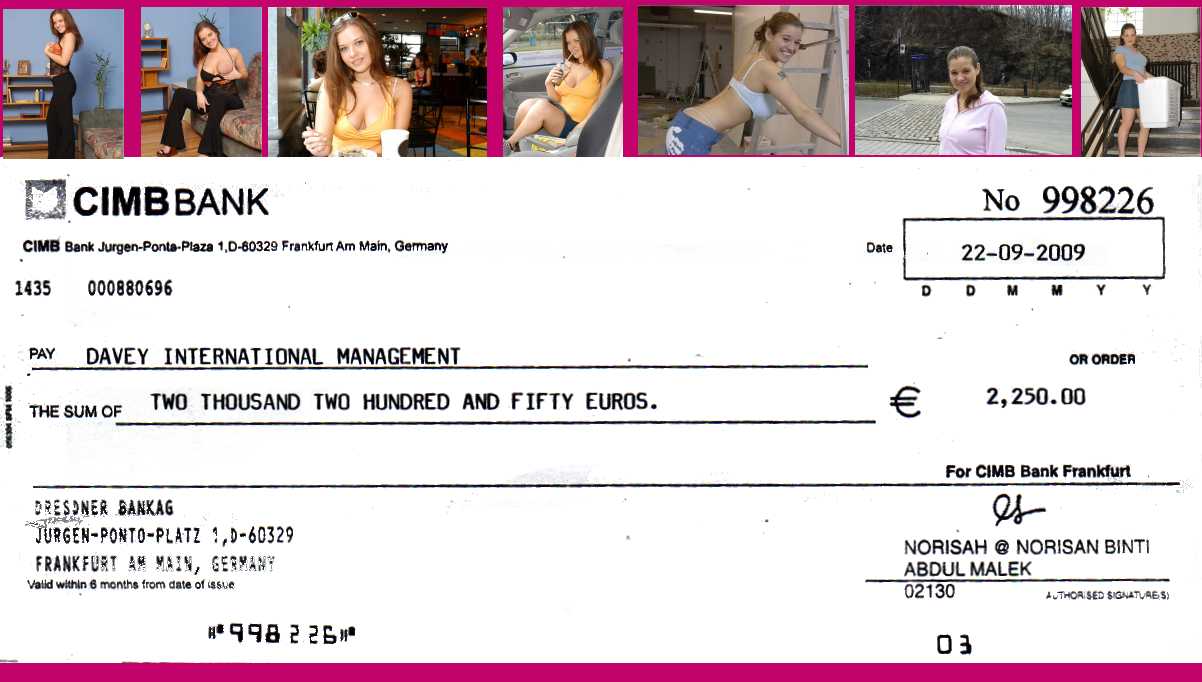

for her. By now we knew a scam was

coming. So we gave a dormant account

name with 1p in it! 2

days later an envelope addressed to

thecompany, posted special delivery,

arrived. It

was, as shown above, in Euros in the

sum of 2,250 Euros. |

On the day of

arrival it was banked & the bank

stated that there could be up to 5

weeks to clear the cheque as it was

in a foreign currency. So we sent a

copy to the Connerz bank which now

owns the CIMBBANK. Well the weekend

passed and on Monday Miss Robinson

said she was to come the following

Thursday and could our would-be

sucker advance her the £720 for her

air ticket! This is when the

scam was confirmed as she said we

should take it out of the proceeds

of the cheque when it was cleared.

We already knew it would never

clear. So we asked her to get her

travel agent to contact us.He never

did. The details of Miss Robinson

are below. It could have been an

expensive view of a tit!

|

| Email:

Sharon Robinson sharon.robinson871@gmail.com.

|

Phone

No +27833665908. |

Skype

No:Shally 435 |

|

Liberty

is

"when some perfectly

respectable person gets up and

says something everybody

agrees to, " while "license is

when some infernal scoundrel,

who ought to be hanged anyway,

gets up and says something

that is true."

Liberty

is

"when some perfectly

respectable person gets up and

says something everybody

agrees to, " while "license is

when some infernal scoundrel,

who ought to be hanged anyway,

gets up and says something

that is true."

So

it

was John Wilkes—radical

journalist, member of Parliament,

outlaw, prisoner, lord mayor of

London, and self-described

libertine in the 18th century. His

life and career go a long way

toward dispelling the superstition

that liberty must advance hand in

glove with order, guided by men of

sterling moral character. Probably

born in 1726 (the exact year is

uncertain), Wilkes clashed with

George III and his ministers

. In John

Wilkes, his

new biography, Arthur H. Cash

shows us why lovers of

liberty, at least, should

celebrate this colourful

Englishman. Cash tells his readers

from the outset, "If you think the

police have the right to arrest

forty-nine people when they are

looking for three, shut [this

book] now."

With

this in mind Shitstirrers

read this notice from the Arthur

Daley's down at the Winchester

Club to ourselves amongst others

and realised that so-called

"freedom of speech" and action is

once more being challenged. So

much in the spirit of John

Wilkes's No 45 The North Briton we

are hereby challenging the

Winchester Club in their authority

to try and curb freedom of speech

.

We have informed them and their

Chairman of our actions and will

publish any response or legal

action that ensues. At

present we just publish their

letter and our response.

The relevant Members of

Parliament in Hampshire are

who invited to look into

this are: Aldershot

Gerald

Howarth (Con), Basingstoke

Andrew

Hunter (Con), East

Hampshire

Michael Mates (Con), Eastleigh

David

Chidgey (LDem), Fareham

Mark

Hoban (Con), Gosport

Peter

Viggers (Con), Havant

David

Willetts (Con), New Forest

East

Dr Julian Lewis (Con), New Forest

West

Desmond Swayne (Con), North East

Hampshire

Rt Hon James Arbuthnot (Con), North West

Hampshire

Rt

Hon Sir George Young Bt (Con), Portsmouth

North

Syd Rapson BEM (Lab), Portsmouth

South

Mike Hancock CBE (LDem), Romsey

Sandra

Gidley (LDem), Southampton

Itchen

Rt Hon John Denham (Lab), Southampton,

Test

Dr Alan Whitehead (Lab) and Winchester

Mark

Oaten (LDem). Every Local

Councillor in Hampshire

should question such action too.

From

The Winchester Club

Our

Response

Email:

drummondco@drummondco.idps.co.uk

Website: www.ukinformedinvestor.co.uk

A.Havlin

Esq.

Legal Practice,Chief

Executive’s Department

The Castle

WINCHESTER

Hampshire

SO23 8UJ

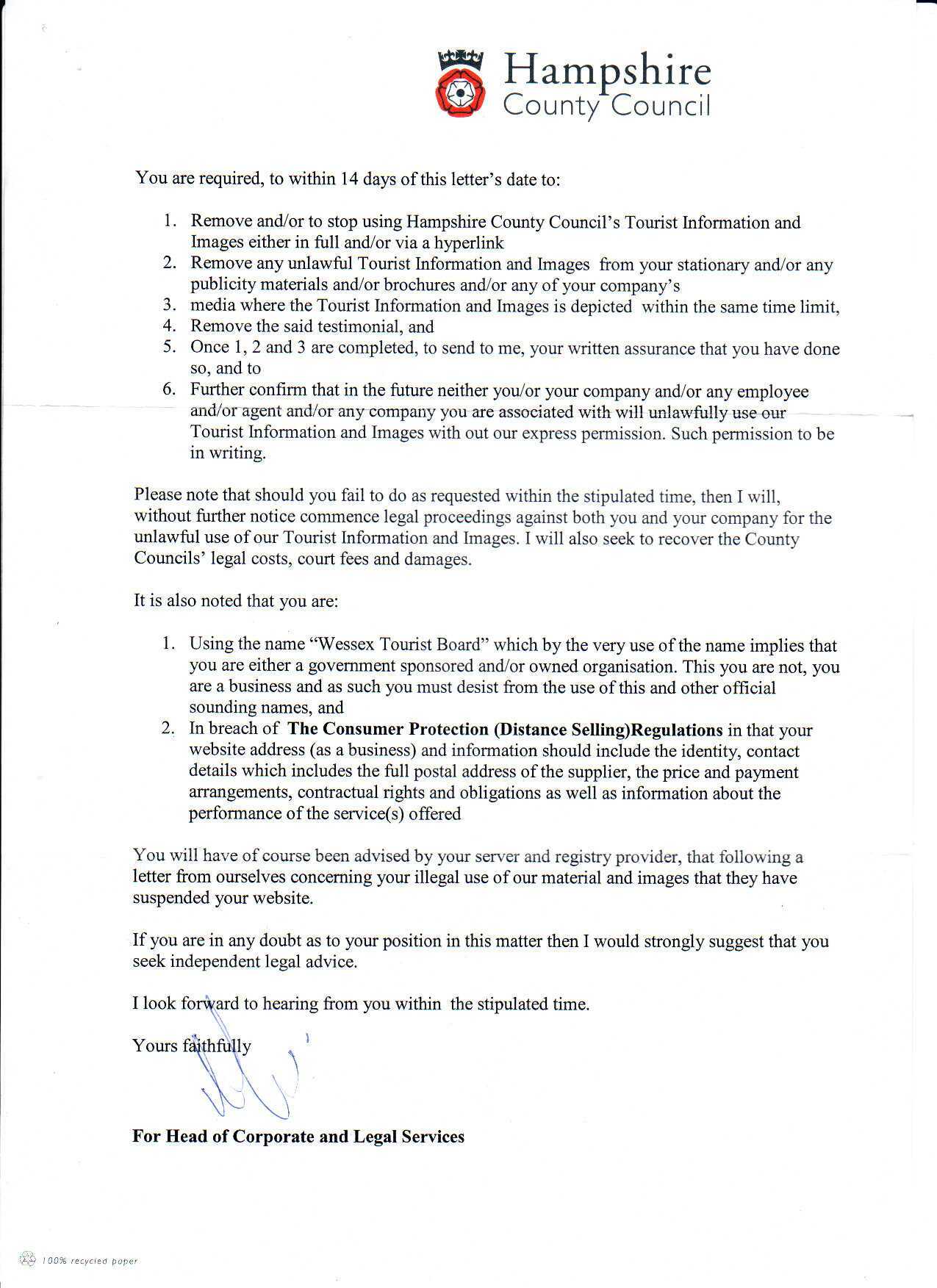

Thursday, 20 November

2008

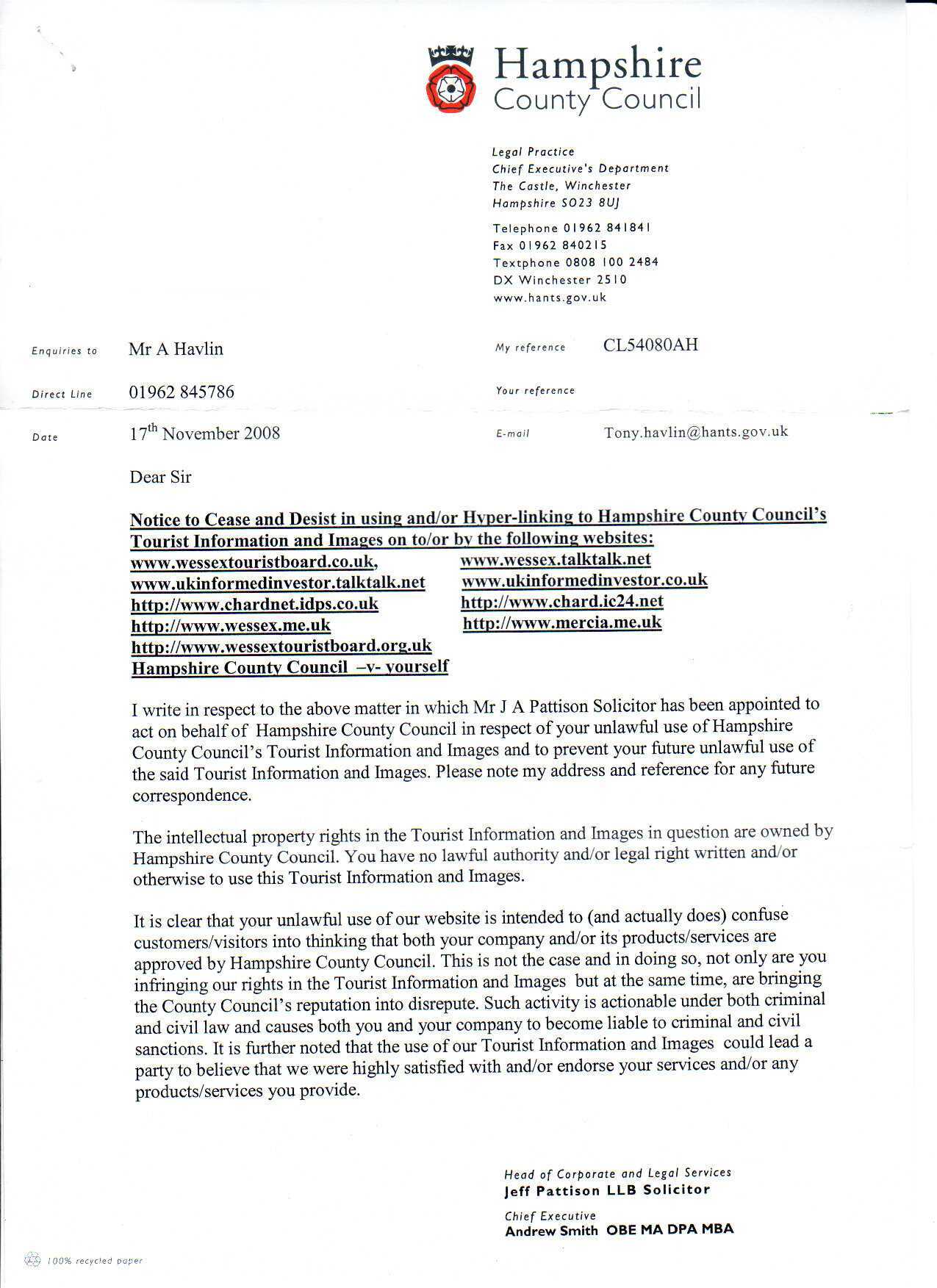

Ref:

CL54080AH

Dear Mr.

Havlin

YOUR

NOTICE

We thank

you for your posted

Notice received today

We still do not

comprehend your blanket

notice as most of the

sites you mention have

no mention or reference

or carry any images in

regards to Hampshire

County Council

whatsoever. Please

inform us of any

specific image or

information that you

consider unlawful. As

the sites www.ukinformedinvestor.co.uk,

www.wessextouristboard.co.uk and www.mercia.me.uk

carry no mention of

Hampshire or show any

images of Hampshire

other than one of many

1000s of click throughs

to websites I cannot

understand any relevance

in this matter other

than to intimidate.

In fact

the only page on all our

sites that made any

reference to the

Hampshire County Council

is www.wessex.me.uk/HampshireAttractions.html We,

shall comply with your

notice in regards

anything you

specifically request to

be changed or removed on

that page as a courtesy,

even though we did

enquire in regards to

this in 2003 before it

was written and we

acknowledge your

assistance. The site was

www.chardnet.co.uk

at that time. So please

identify that which you

consider is your

intellectual property

and we will re-write and

/or replace images. We

await your further &

better particulars on

the relevant sites and

then we will comply

within 14 days on any

proven breach of

intellectual property

However

we

are quite prepared to

accept legal proceedings

and get a legal decision

on the other matters,

which we believe have no

legal standings

whatsoever. We have

placed the following on

the page mentioned above

as follows:

“This

section has been a

feature of this part of

Wessex since it was

written 4/5 years ago (

when our site was

www.chardnet.co.uk).

Unfortunately the

Hampshire County Council

has issued a NOTICE

TO CEASE & DESIST

IN USING AND/OR

HYPERLINKING TO

HAMPSHIRE COUNTY

COUNCIL'S TOURIST

INFORMATION AND IMAGES

ONTO/OR BY THIS SITE and

others & tried

to influence 3rd

parties. They claim that

unspecified parts are

their "intellectual

"property & must be

removed. But have failed

to specify which parts.

It is our intention to

continue

to

show

this search engine to

assist visitors and

defend our right of free

speech. We have, until

now, published an

acknowledgement to

Hampshire County Council

just here and referred

people to their site.

This it seems has

created offence as have

our other sites, which

have been specified,

which are financial,

legal and commercial and

have never shown

anything pertaining to

Hampshire County

Council. Our sites have

been on-line since 1999

and date back through

other means of media to

1972. These thumbnails

are a means of direction

to the various websites

and are not a copy of

"War & Peace" lifted

from Tolstoy! No charges

have ever been levied

for our information

services. We shall be

publishing the

correspondence for

readers to judge on our

Shitstirrers of Wessex

page and the UK Informed

Investor will now be

mentioning it on their

Watchdog page. It shall

also be brought to the

notice of people of

influence. We always

name names. Details of

our breach(es) of

"Intellectual" Property

"MAY BE"

available from

the Tony Havlin, Jeff

Pattison and Andrew

Smith at The Castle

Winchester, Hampshire

SO23 8UJ. Tel:01962

841841. Fax: 01962

840215 Email: Tony.havlin@hants.gov.uk.

Once identified they

will be replaced by

this notice as

requested and all the

thumbnails will be

rounded off. We

apologise to the

attraction owners if

this means they have

fewer visitors as over

35 million page visits

to our sites

have been made, and

over 25 million in

2008 so far. The

domain names of

www.wessex.me.uk and

www.wessextouristboard.org.uk

have been properly

registered. There is

no legal definition of

the words "Tourist

Board" or prohibition

for the use of such

titles or a law

to prohibit

hyper-linking from the

site as they have

tried to intimate. If

so we note they are

listed on many other

search engines with

hyper-links. Maybe the

Government will stop

the "Ministry of

Sound" nightclub or

the "Ministry of

Cakes" in Taunton,

Somerset.

We

also

point out that we have

complied with The

Consumer Protection

(Distance Selling)

Regulations by placing

the “contact us”

hyperlink on each page

and that hyperlink goes

to the page where the

details are lodged.

As for

the name Wessex Tourist

Board. This has been

properly registered and

accepted. We shall not

desist from using the

name unless so ordered

by a Court of Law.

Please advise us of any

legislation that you

believe enhances your

telling us to desist

from using that name. We

have for many years now

been assisting readers

both by email and on the

telephone with

information in regards

to Tourism in both

Wessex and Mercia.

Especially when local

tourist offices are

closed on Saturday

afternoons and Sundays.

This has been done free

of charge and

courteously. We

fail

to see what this has to

do with the Hampshire

County Council. As we do

not charge the matter of

fees is immaterial. We

are a firm of European

Tax and Legal advisers

who have created

reference pages as a

service and it is in the

fields of legal and tax

advice that we have

charged since 1966. The

fees are dependant on

the advice we give and

the work done.

Interference

with

us carrying on our

legitimate business , if

this continues, will be

counterclaimed if you

continue to proceed with

legal action.

It

has

always been our

intention to work in

harmony and co-operation

and a simple call or

request in the first

instance would have been

dealt with to everyone’s

satisfaction. You made

no such approach . We

are still open to

constructive discussion.

We do reserve the right

to publish the

correspondence on our

sites for the

consideration of our

readers, as we always do

whether it be with large

corporations, local

councils, Insurance

Companies, Government

Offices or the public.

We have a “Watchdog

Column” on our financial

site, which is usually

picked up by the media.

Assuring

you

of our services at all

times.

Faithfully

yours,

Drummond

& Co.

|

The Wessex Tourist

Board Kiosks will be

opening at Easter 2009

in conjunction with a

major Hotel Group. They

will be open 7 days a

week 9am-9pm and will

include services to

visitors never before

available from Tourist

Offices. There will be

three in Hampshire!

|

|

|

CEO

E-mail addresses

So,

you're

fed up dealing with "Customer Services"

on general-purpose contact e-mail

addresses. Are you not getting replies,

or not getting the replies you want?

Time to take it to the top! Chief

Executive Officers (CEOs) are very

reluctant to publish their e-mail

addresses. This page attempts to redress

the balance by publishing the e-mail

addresses for the CEOs of some UK

companies, government and other

organisations. We believe in letting the

"little people" get noticed. It

seems that this column has upset some

people. We believe in transparency and

publishing what is already in the public

domain. two Companies have complained to

our providers that we list them...

they are Dreams The bed Company &

Hillary's the Blind people. Whilst we

hve had dealings with Dreams and may

well be publishing a case of alleged

unfair dismissal of a member of staff

which is going before a tribunal, we

have had no dealings with Hillarys. we

have also been approached by a company

who represent directline-the Insurance

people. Their reason is concerns about

Google's policy of demoting a company

that have too many listings.

Whilst we appreciate the sentiments this

is nothing more than a restrictive

practice within the advertising

industry...which is illegal. Most

of those listed have websites, advertise

and tout for business. Our information

is gleaned from those sources as well as

public listings. They aretherefore in

the public domain.

Obviously some people have had a go at

the providers of the list Ceomail as

they have written to ask us to remove

this section. THIS WE WILL NOT

DO.... the public have the right to

avail themselves of such information...

so we are going to extend create

our own extensive list and mention those

companies we have had complaints about.

In fairness we shall commend those

companies or institutions who have acted

properly and rectified problems. Amongst

those wecommend are BT, Talk talk,

Vodafone, Orange(EE) and Plusnet. Also

David Laws MP, Jeremy Browne MP , Grant

ShappsMP and Oliver Letwin MP. We thank

Ceomail for their assistance in the

past.

Some tips when e-mailing:

- Be polite

- Keep the information concise and

to the point

- Include customer reference

numbers or invoice numbers, if

applicable

- Include a brief history of the

issue, if applicable

- Do not accept being passed back

to "Customer Services" or elsewhere

within the organisation

- Insist on a reply from the CEO

If you're working as part of a campaign

group, send a personal, individually-created

letter. Letters which are cut/pasted from a

standard template will invariably receive a

standard template response in reply... Good

luck with your enquiry!

|

Contact your Councillors, MP,

MEPs,

MSPs,

or Northern Ireland, Welsh and

London AMs for

free

Do you need help

with

your postcode?

|

UK

Companies

| Company Name |

CEO Name |

CEO E-mail Address |

Website |

FTSE Symbol |

Last Verified |

| Agro-Food

&

Drinks |

|

|

|

|

|

| Associated British

Foods |

George Weston, Chief

Executive |

georgeweston@abfoods.com |

http://www.abf.co.uk |

ABF.L

(FTSE100) |

16 Jun 2010 |

| Cadbury-Schweppes |

Todd Stitzer, Chief

Executive |

Todd.Stitzer@csplc.com |

http://www.cadburyschweppes.com |

CBRY.L

(FTSE100) |

16 Jun 2010 |

| Dairy Crest |

Mark Allen, Chief

Executive |

mark.allen@dairycrest.co.uk |

http://www.dairycrest.co.uk |

DCG.L

(FTSE250) |

16 Jun 2010 |

| Diageo |

Paul

Walsh, Chief Executive |

paul.s.walsh@diageo.com |

http://www.diageo.com |

DGE.L

(FTSE100) |

16 Jun 2010 |

| Dominos UK |

Chris Moore, Chief

Executive |

chris.moore@dominos.co.uk |

http://www.dominos.co.uk

Tel: 01908 580604 |

|

21 Sep 2010 |

| Fyffes |

David McCann,

Chairman |

dmccann@fyffes.com |

http://www.fyffes.com |

(Ireland) |

16 Jun 2010 |

| Kelloggs UK |

Greg Peterson,

Managing Director, UK |

greg.peterson@kellogg.com |

http://www.kelloggs.co.uk |

|

16 Jun 2010 |

| KFC UK |

Martin Shuker,

Managing Director |

martin.shuker@yum.com |

http://www.kfc.co.uk |

Part of Yum! Brands |

16 Jun 2010 |

| McDonalds UK |

Steve Easterbrook,

Chief Executive |

steve.easterbrook@uk.mcd.com |

http://www.mcdonalds.co.uk |

|

16 Jun 2010 |

| Pizza Express UK |

Mark Angela,

Managing Director |

mark.angela@pizzaexpress.com |

http://www.pizzaexpress.com |

|

16 Jun 2010 |

| Pizza Hut UK |

Jens Hofma, Managing

Director |

jens.hofma@pizzahut.co.uk |

http://www.pizzahut.co.uk |

Part of Yum! Brands |

16 Jun 2010 |

| Unilever |

Paul Polman, Chief

Executive |

Paul.Polman@unilever.com |

http://www.unilever.com |

ULVR.L

(FTSE100) |

16 Jun 2010 |

| Whitbread

(Beefeater, Brewers Fayre, Costa,

Premier Inn) |

Andy Harrison, Chief

Executive |

andy.harrison@whitbread.com |

http://www.whitbread.co.uk/ |

WTB.L |

1 Sep 2010 |

| Automobiles |

|

|

|

|

|

| Audi UK |

Jeremy Hicks,

Director |

jeremy.hicks@audi.co.uk |

http://www.audi.co.uk |

|

16 Jun 2010 |

| Bentley UK |

Franz-Josef Paefgen,

Director |

franz-josef.paefgen@bentley.co.uk |

http://www.bentley.co.uk |

|

16 Jun 2010 |

| BMW UK |

Tim Abbott, Managing

Director |

tim.abbott@bmw.co.uk |

http://www.bmw.co.uk |

|

16 Jun 2010 |

| Ford UK |

Nigel Sharp,

Managing Director |

nsharp@ford.com |

http://www.ford.co.uk |

|

16 Jun 2010 |

| Honda UK |

Ken Keir, Managing

Director |

ken.keir@honda.co.uk |

http://www.honda.co.uk |

|

3 Sep 2010 |

| Jaguar Land Rover |

Carl-Peter Forster,

Chief Executive |

pforster@jaguarlandrover.com |

|

Part of Tata Motors |

28 May 2010 |

| Land Rover |

Phil Popham,

Managing Director |

ppopham@jaguarlandrover.com |

|

Part of JLR / Tata

Motors |

28 May 2010 |

| Manganese Bronze

(Taxis) |

John Russell, Group

Chief Executive |

jrussell@manganese.com |

http://www.manganese.com |

|

28 Jun 2010 |

| Mercedes-Benz UK |

Simon Oldfield,

Managing Director Customer Services |

simon.oldfield@daimler.com |

http://www.mercedes-benz.co.uk/ |

|

6 Aug 2010 |

| Mitsubishi UK |

Lance Bradley,

Managing Director |

l.bradley@mitsubishi-cars.co.uk |

http://www.mitsubishi-cars.co.uk |

|

21 Jul 2010 |

| Nissan UK |

Paul Willcox,

Managing Director |

paul.willcox@nissan.co.uk |

http://www.nissan.co.uk |

|

29 Mar 2010 |

| Peugeot UK |

Jonathan Goodman,

Managing Director |

jonathan.goodman@peugeot.com |

http://www.peugeot.co.uk |

|

8 Jun 2010 |

| Porsche GB |

Andy Goss, Managing

Director |

andy.goss@porsche.co.uk |

http://www.porsche.co.uk |

|

29 Mar 2010 |

| Renault UK |

Roland Bouchaea,

Managing Director |

roland.bouchara@renault.com |

http://www.renault.co.uk |

|

14 Sep 2010 |

| Rolls-Royce Motor

Cars |

Torsten

Müller-Ötvös, Chief Executive |

|

http://www.rolls-roycemotorcars.com |

Part of BMW |

3 Mar 2010 |

| Toyota UK |

Miguel Fonseca,

Managing Director |

miguel.fonseca@tgb.toyota.co.uk |

http://www.toyota.co.uk |

|

21 Feb 2010 |

| Vauxhall / Opel UK |

Nick Reilly, Chief

Executive |

nick.reilly@gm.com |

http://www.vauxhall.co.uk |

|

9 Feb 2010 |

| Volkswagen UK |

Chris Craft,

Director |

chris.craft@volkswagen.co.uk |

http://www.volkswagen.co.uk |

|

29 Mar 2010 |

| Volvo UK |

Peter Rask, Managing

Director |

prask@volvocars.com |

http://www.volvocars.com/uk |

Part of Zhejiang

Geely Holding Group |

3 Apr 2010 |

| Charities

|

|

|

|

|

|

| Arts Council |

Alan Davey, Chief

Executive |

alan.davey@artscouncil.org.uk |

|

|

26 Sep 2010 |

| Barnardo's |

Martin Narey, Chief

Executive |

martin.narey@barnardos.org.uk |

|

|

26 Sep 2010 |

| British Heart

Foundation |

Peter Hollins, Chief

Executive |

hollinsp@bhf.org.uk |

|

|

26 Sep 2010 |

| Cancer Research UK |

|

|

|

|

26 Sep 2010 |

| National Trust |

|

|

|

|

26 Sep 2010 |

| Oxfam |

Barbara Stocking,

Chief Executive |

bstocking@oxfam.org.uk |

|

|

26 Sep 2010 |

| RSPB |

Graham Wynne, Chief

Executive |

graham.wynne@rspb.org.uk |

|

|

26 Sep 2010 |

| RSPCA |

Mark Watts, Chief

Executive |

mwatts@rspca.org.uk |

|

|

26 Sep 2010 |

| Salvation Army |

|

|

|

|

26 Sep 2010 |

| Scope |

Richard Hawkes,

Chief Executive |

richard.hawkes@scope.org.uk |

|

|

26 Sep 2010 |

| Wellcome Trust |

|

|

|

|

26 Sep 2010 |

| Chemicals |

|

|

|

|

|

| BOC Group |

Mike Huggon,

Managing Director |

janet.sheldrick@boc.com

(PA) |

http://www.boc.com |

Part of the Linde

Group |

3 Mar 2010 |

| ICI |

John McAdam, Chief

Executive |

john_mcadam@ici.co.uk |

http://www.ici.co.uk |

ICI.L

(FTSE100) |

|

| Reckitt Benckiser |

Bart Becht, Chief

Executive |

|

http://www.rb.com |

RB.L

(FTSE100) |

4 Jan 2010 |

| Construction &

Building |

|

|

|

|

|

| Balfour Beatty |

Ian Tyler, Chief

Executive |

ian.tyler@balfourbeatty.com |

http://www.balfourbeatty.com |

|

16 Sep 2010 |

| EAGA Insulation |

Drew Johnson, Chief

Executive |

drew.johnson@eaga.com |

http://www.eaga.com |

|

21 Aug 2010 |

| Travis Perkins

(Wickes, Toolstation, Tile Giant,

Benchmarx) |

Geoff Cooper, Chief

Executive |

geoff.cooper@travisperkins.co.uk |

http://www.travisperkins.co.uk |

|

24 Sep 2010 |

| Wain Homes |

Steve Toghill, Chief

Executive |

steve.toghill@wainhomes.net |

http://www.wainhomes.net |

|

21 Aug 2010 |

| Distribution |

|

|

|

|

|

| Alliance Boots |

Andy Hornby, Chief

Executive |

andy.hornby@allianceboots.com |

http://www.allianceboots.com |

Privately held |

17 May 2010 |

| Arcadia Group

(Burton, Dorothy Perkins, Evans,

Miss Selfridge, Topman, Topshop,

Wallis) |

Ian Grabiner, Chief

Executive |

ian.grabiner@arcadiagroup.co.uk |

http://www.arcadiagroup.co.uk |

|

21 Feb 2010 |

| Argos |

Sara Weller,

Managing Director |

sara.weller@argos.co.uk |

http://www.argos.co.uk |

Part of Home Retail

Group |

24 Jan 2010 |

| ASDA |

Andy Clarke, Chief

Executive |

andy.clarke@asda.co.uk |

http://www.asda.co.uk |

Part of Wal-Mart |

21 May 2010 |

| Boots |

Stefano Pessina,

Executive Chairman |

stefano.pessina@allianceboots.com |

http://www.allianceboots.com |

Part of Alliance

Boots |

|

| Burberry Group |

Angela Ahrendts,

Chief Executive |

angela.ahrendts@burberry.com |

http://www.burberry.com |

BRBY.L

(FTSE100) |

21 Feb 2010 |

| Co-operative

Group

(Co-op) |

Peter Marks, Chief

Executive |

peter.marks@co-operative.coop |

http://www.co-operative.coop |

Mutual |

2 Dec 2009 |

| Comet |

Hugh Harvey,

Managing Director |

hugh.harvey@comet.co.uk |

http://www.comet.co.uk |

Part of KESA

Electricals Group |

30 Mar 2010 |

| Damart |

Andy Hill, Chief

Executive |

ahill@damart.co.uk |

http://www.damart.co.uk/ |

|

16 Sep 2010 |

| Debenhams |

Rob Templeman, Chief

Executive |

rob.templeman@debenhams.com |

http://www.debenhams.com |

DEB.L (FTSE250) |

21 Feb 2010 |

| Dreams Beds |

Nick Worthington,

Chief Executive |

nickworthington@dreams.co.uk |

http://www.dreams.co.uk |

|

21 Aug 2010 |

| Dixons Group /

Currys / PC World |

John Browett, Chief

Executive |

john.browett@dixons.co.uk |

http://www.dixons.co.uk |

DXNS.L |

28 Oct 2009 |

| Flying Flowers |

Stephen Cook, Chief

Executive |

scook@flyingbrands.com |

http://www.flyingflowers.co.uk |

|

30 Oct 2009 |

| Freeman Grattan

Holdings (includes Freemans, Grattan

& Lookagain) |

Koert Tulleners,

Chief Executive |

koert.tulleners@fgh-uk.com |

|

|

13 Apr 2010 |

| GAME Group PLC |

Lisa Morgan, Chief

Executive |

lisa.morgan@game.co.uk |

http://www.gamegroup.plc.uk/ |

|

7 Feb 2010 |

| Glen Dimplex

(Belling, Burco, Carmen, Creda,

Dimplex, Goblin, LEC, Morphy

Richards, Xpelair) |

Sean O'Driscoll,

Chief Executive |

sean.odriscoll@glendimplex.com |

http://www.glendimplex.com |

|

24 Mar 2010 |

| Greggs |

Ken McMeikan, Chief

Executive |

ken.mcmeikan@greggs.co.uk

|

http://www.greggs.co.uk |

GRG.L

(FTSE250) |

10 Feb 2010 |

| Halfords |

David Wild, Chief

Executive |

david.wild@halfords.co.uk |

http://www.halfords.co.uk |

|

25 Jan 2010 |

| Hillarys Blinds |

John Risman, Chief

Executive |

john.risman@hillarys.co.uk |

http://www.hillarys.co.uk |

|

19 Sep 2010 |

| Home Retail Group

(Argos and Homebase) |

Terry Duddy, Chief

Executive |

terry.duddy@homeretailgroup.com

|

http://www.homeretailgroup.com |

HOME.L

(FTSE100) |

23 Feb 2010 |

| Homebase |

|

|

http://www.homebase.co.uk |

Part of Home Retail

Group |

10 Feb 2010 |

| House of Fraser |

John King, Chief

Executive |

jking@hof.co.uk |

http://www.houseoffraser.co.uk/ |

|

16 Sep 2010 |

| Iceland |

Malcolm Walker,

Chief Executive |

malcolm.walker@iceland.co.uk |

http://www.iceland.co.uk |

Part of Baugur |

|

| JD Sports |

Barry Bown, Chief

Executive |

barry.bown@jdplc.com |

http://www.jdsports.co.uk |

|

8 Jun 2010 |

| Jessops |

Trevor Moore, Chief

Executive |

tmoore@jessops.com |

http://www.jessops.com |

|

22 Sep 2010 |

| JJB Sports |

Keith Jones, Chief

Executive |

kjones@jjbsports.com |

http://www.jjbsports.com |

|

23 Mar 2010 |

| John Lewis

Partnership |

Andy Street, Chief

Executive |

andy_street@johnlewis.co.uk |

http://www.johnlewis.co.uk |

|

17 May 2010 |

| Kingfisher (B&Q

and Screwfix) |

Ian Cheshire, Chief

Executive |

ian.cheshire@kingfisher.com |

|

KGF.L |

25 Mar 2010 |

| Kwik-Fit |

Ian Fraser, Chief

Executive |

ian.fraser@kwik-fit.com |

http://www.kwik-fit.com |

|

9 Apr 2010 |

| Laura Ashley |

Lillian Tan, Chief

Executive |

lillian.tan@lauraashley.com |

http://www.lauraashley.com |

|

21 Feb 2010 |

| Marks & Spencer |

Marc Bolland, Chief

Executive |

marc.bolland@marks-and-spencer.com |

http://www.marksandspencer.com |

MKS.L

(FTSE100) |

11 Aug 2010 |

| Morphy Richards |

Phil Green, Chief

Executive |

phil.green@morphyrichards.co.uk |

http://www.morphyrichards.co.uk |

part of Glen Dimplex |

24 Mar 2010 |

| Morrisons |

Dalton Philips, CEO |

dalton.philips@morrisonsplc.co.uk |

http://www.morrisons.co.uk |

MRW.L

(FTSE100) |

24 May 2010 |

| Mothercare |

Ben Gordon, Managing

Director |

ben.gordon@mothercare.co.uk |

http://www.mothercare.com |

|

30 Mar 2010 |

| Next |

Simon Wolfson, Chief

Executive |

simon.wolfson@nextplc.co.uk |

|

NXL.L (FTSE100) |

29 May 2010 |

| Ocado |

Tim Steiner, Chief

Executive |

Tim.steiner@ocado.com |

http://www.ocado.com |

Partly owned by John

Lewis Partnership |

3 Sep 2009 |

| Paperchase |

Timothy

Elliot-Murray-Kynynmound |

timothy@paperchase.co.uk |

http://www.paperchase.co.uk |

|

11 Feb 2010 |

| Peter Jones |

Simon Fowler,

Managing Director |

simon_fowler@johnlewis.co.uk |

|

Part of John Lewis

Partnership |

26 Mar 2010 |

| play.com |

John Perkins, Chief

Executive |

john.perkins@play.com |

http://www.play.com |

|

3 Jun 2010 |

| Sainsbury |

Justin King, Chief

Executive |

justin.king@sainsburys.co.uk |

http://www.sainsbury.co.uk |

SBRY.L

(FTSE100) |

3 Sep 2009 |

| Shop Direct (Empire

Stores, Great Universal, Kays,

Littlewoods, Very, Marshall Ward,

Woolworths) |

Mark Newton-Jones,

Chief Executive |

mark.newton-jones@shopdirect.com |

http://www.shopdirect.com |

|

8 Jun 2010 |

| Somerfield |

|

|

http://www.somerfield.co.uk |

Part of Co-operative

Group |

10 Dec 2009 |

| Specsavers |

John Perkins, Chief

Executive |

dougp@uk.specsavers.com |

http://www.specsavers.co.uk |

|

14 Sep 2010 |

| Sports Direct |

Dave Forsey, Chief

Executive |

Dave.Forsey@sportsdirect.com |

http://www.sportsdirect.com |

|

22 Apr 2010 |

| Staples |

Peter Birks, VP UK

& Ireland |

peter.birks@staples.co.uk |

http://www.staples.co.uk |

|

24 Jan 2010 |

| Steinhoff Group /

Homestyle / Harveys / Benson for

Beds / Sleepmaster / Cargo |

Markus Jooste, Chief

Executive |

markus.jooste@steinhoff.co.za |

http://www.sukf.co.uk |

|

14 Sep 2010 |

| Tesco |

Terry Leahy, Chief

Executive |

terry.leahy@uk.tesco.com |

http://www.tesco.com |

TSCO.L

(FTSE100) |

27 Nov 2009 |

| Thorntons |

Mike Davies, Chief

Executive |

mike.davies@thorntons.co.uk |

http://www.thorntons.co.uk |

|

5 Feb 2009 |

| Toolstation |

Mark Goddard-Watts,

Chief Executive |

mark@toolstation.com |

http://www.toolstation.com |

|

21 Aug 2010 |

| Waitrose |

Mark Price, Managing

Director |

mark_price@waitrose.co.uk |

http://www.waitrose.co.uk |

Part of John Lewis

Partnership |

8 Oct 2009 |

| WH Smith |

Kate

Swann, Chief Executive |

kate.swann@whsmith.co.uk |

http://www.whsmith.co.uk |

|

19 Feb 2010 |

| Electrical

& Electronics |

|

|

|

|

|

|

| Canon UK |

|

|

http://www.canon.co.uk |

|

22 Sep 2010 |

| Indesit UK

(Hotpoint, Indesit, Cannon &

Creda) |

Enrico Vita, Chief

Executive |

enrico.vita@indesit.com |

http://www.indesit.co.uk |

|

16 Sep 2010 |

| LG UK |

Brian Na, President |

brian.na@lge.com |

http://www.lge.co.uk |

|

16 Sep 2010 |

| Nikon UK |

Michio Miwa,

President |

Michio.Miwa@nikon.co.uk |

http://www.nikon.co.uk |

|

22 Sep 2010 |

| Finance and

Insurance |

|

|

|

|

|

| AEGON Scottish

Equitable |

Otto Thoresen, Chief

Executive |

Otto.Thoresen@aegon.co.uk |

http://www.aegon.co.uk |

|

24 Jan 2010 |

| Alliance &

Leicester |

|

|

http://www.alliance-leicester.co.uk |

Part of Santander

Group |

10 Dec 2009 |

| American Express UK |

Raymond Joabar,

Country Manager |

raymond.joabar@aexp.com |

http://www.americanexpress.co.uk |

|

9 Aug 2010 |

| Aviva and Royal

Automobile Club (RAC) |

Andrew Moss, Chief

Executive |

andrew_moss@aviva.com |

http://www.aviva.com |

AV.L

(FTSE100) |

21 Aug 2010 |

| AXA UK |

Nicolas

Moreau, Chief Executive |

nicolas.moreau@axa.co.uk |

|

|

18 Feb 2010 |

| Bank of England |

Mervyn King,

Governor |

mervyn.king@bankofengland.co.uk |

http://www.bankofengland.co.uk |

|

10 Feb 2010 |

| Barclaycard |

Amer Sajed, Managing

Director |

amer.sajed@barclaycard.co.uk |

http://www.barclaycard.co.uk |

|

20 Sep 2010 |

| Barclays |

John Varley, Chief

Executive |

john.varley@barclays.com |

http://www.barclays.co.uk |

BARC.L

(FTSE100) |

10 Nov 2009 |

| Bradford &

Bingley |

Richard Banks,

Managing Director |

richard.banks@bbg.co.uk |

http://www.bradford-bingley.co.uk |

Nationalised |

19 March 2010 |

| Britannia Building

Society |

|

|

|

Part of Co-Operative

Group |

10 Dec 2009 |

| Britannic |

Paul Thompson, Chief

Executive |

thompsonp@britannic.co.uk |

|

Part of Pearl Group |

|

| Callcredit

Information Group |

John McAndrew, Chief

Executive |

john.mcandrew@callcredit.co.uk |

http://www.callcredit.co.uk |

|

1 May 2010 |

| Camelot Group

(National Lottery) |

Dianne Thompson,

Chief Executive |

dianne.thompson@camelotgroup.co.uk |

http://www.camelotgroup.co.uk |

|

9 Feb 2010 |

| Clydesdale Bank |

Lynne Peacock, Chief

Executive |

Lynne.Peacock@cbonline.co.uk |

http://www.cbonline.co.uk |

Part of National

Australia Bank |

16 Dec 2009 |

| Co-operative

Financial

Services / Co-op Bank |

Neville Richardson,

Chief Executive |

neville.richardson@cfs.coop |

http://www.co-operativebank.co.uk |

Mutual |

8 Mar 2010 |

| Deutsche Bank UK |

Colin Grassie, Chief

Executive |

colin.grassie@db.com |

http://www.db.com |

|

21 Jul 2010 |

| Egg |

Bert Pijls, Chief

Executive |

bert.pijls@citi.com |

http://www.egg.com |

Part of Citibank |

30 Mar 2010 |

| Equifax |

Sandra Lawrence, UK

General Manager |

sandra.lawrence@equifax.com |

http://www.equifax.co.uk |

|

19 Apr 2010 |

| Esure / Sheila's

Wheels |

Peter Wood, Chief

Executive |

peter.wood@esure.com |

http://www.esure.com |

|

1 Sep 2010 |

| Experian / Credit

Expert |

Don Robert, Chief

Executive |

don.robert@uk.experian.com |

http://www.experian.co.uk

020 3042 4215 |

EXPN.L

(FTSE100) |

21 Sep 2010 |

| First Direct |

Chris Pilling, Chief

Executive |

chrispilling@firstdirect.com |

http://www.firstdirect.com |

Part of HSBC |

25 May 2010 |

| Friends Provident |

Trevor Matthews,

Chief Executive |

trevor.matthews@friendsprovident.co.uk |

http://www.friendsprovident.co.uk |

FP.L

(FTSE100) |

|

| HSBC UK |

Paul Thurston, Chief

Executive |

managingdirectoruk@hsbc.com |

http://www.hsbc.co.uk |

HSBA.L

(FTSE100) |

|

| ICICI Bank UK |

Suvek Nambiar,

Managing Director |

suvek.nambiar@icicibank.com |

http://www.icicibank.com |

|

28 May 2010 |

| ING Direct UK |

Richard Doe, Chief

Executive |

richard.doe@ingdirect.co.uk |

http://www.ingdirect.co.uk |

|

23 Sep 2010 |

| Ladbrokes |

Richard Glynn, Chief

Executive |

richard.glynn@ladbrokes.co.uk |

http://www.ladbrokes.co.uk |

|

15 Jul 2010 |

| Legal & General |

Tim Breedon, Chief

Executive |

tim.breedon@group.landg.com |

http://www.landg.com |

LGEN.L

(FTSE100) |

|

| Liverpool Victoria |

Mike Rogers, Chief

Executive |

mike.rogers@lv.com |

http://www.lv.com |

Mutual |

23 Oct 2009 |

| Lloyds TSB (includes

Halifax / Bank of Scotland (HBOS)) |

Eric Daniels, Chief

Executive |

eric.daniels@lloydstsb.co.uk |

http://www.lloydstsb.co.uk |

LLOY.L

(FTSE100) |

2 Sep 2009 |

| Mastercard UK |

Hany Fam, General

Manager |

hany.fam@mastercard.com |

http://www.mastercard.co.uk |

|

26 Sep 2010 |

| MBNA / Bank of

America (UK) |

Ian O'Doherty, Chief

Executive |

ian.odoherty@bankofamerica.com |

|

Part of RBS Group |

5 March 2010 |

| Nationwide |

Graham Beale, Chief

Executive |

gjbeale2@nationwide.co.uk

|

http://www.nationwide.co.uk

(Tel: 01793 513 513 then say "Graham

Beale") |

Mutual |

14 Sep 2010 |

| NatWest |

|

|

|

Part of RBS

Group |

17 Feb 2010 |

| Neovia Financial

(Netbanx, Neteller, Net+) |

Mark Mayhew, Chief

Executive |

mark.mayhew@neovia.com |

http://www.neovia.com |

|

7 Jul 2010 |

| Northern Rock |

Gary Hoffman, Chief

Executive |

gary.hoffman@northernrock.co.uk |

http://www.northernrock.co.uk |

Nationalised |

28 Oct 2009 |

| Prudential |

Tidjane Thiam, Chief

Executive |

tidjane.thiam@prudential.co.uk |

http://www.prudential.co.uk |

PRU.L

(FTSE100) |

4 Jan 2010 |

| Royal & Sun

Alliance (RSA) and "More Than" |

Andy Haste, Chief

Executive |

andy.haste@gcc.rsagroup.com |

http://www.royalsunalliance.com |

RSA.L

(FTSE100) |

2 Sep 2010 |

| Royal

Bank of Scotland (RBS Group) |

Stephen Hester |

Stephen.Hester@rbs.co.uk |

http://www.rbs.co.uk |

RBS.L

(FTSE100) |

8 Feb 2010 |

| Santander

Group (formerly Abbey) |

Antonio Horta-Osorio |

Antonio.Osorio@santander.co.uk |

http://www.santander.co.uk |

|

10 Dec 2009 |

| Scottish Life |

John Deane, Chief

Executive |

jdeane@scottishlife.co.uk |

http://www.scottishlife.co.uk |

|

16 Dec 2009 |

| Skipton Building

Society |

David Cutter, Chief

Executive |

david.cutter@skipton.co.uk |

http://www.skipton.co.uk |

Mutual |

2 Feb 2010 |

| Standard Chartered

Bank |

Peter Sands, Group

Chief Executive |

peter.sands@sc.com |

http://www.standardchartered.com |

STAN.L

(FTSE100) |

10 Feb 2010 |

| Standard Life |

David Nish, Chief

Executive |

david_nish@standardlife.com |

http://www.standardlife.com |

SL.L

(FTSE100) |

10 Feb 2010 |

| Student Loans

Company (SLC) |

Ed Lester, Chief

Executive |

Ed_Lester@slc.co.uk |

http://www.slc.co.uk

Tel: 0141 306 2000 |

|

6 Sep 2010 |

| Yorkshire Building

Society / Chelsea Building Society |

Iain Cornish, Chief

Executive |

iccornish@ybs.co.uk |

http://www.ybs.co.uk |

|

17 Mar 2010 |

| Health &

Pharmaceutical |

|

|

|

|

|

| Amersham |

William Castell,

Chief Executive |

william.castell@amersham.com |

http://www.amersham.com |

|

5 Feb 2009 |

| AstraZeneca |

David Brennan, Chief

Executive |

david.brennan@astrazeneca.com |

http://www.astrazeneca.com |

AZN.L

(FTSE100) |

5 Feb 2009 |

| GlaxoSmithKline |

Andrew

Witty, Chief Executive |

andrew.witty@gsk.com |

http://www.gsk.com |

GSK.L

(FTSE100) |

18 Feb 2010 |

|

IT |

|

|

|

|

|

| ARM Holdings |

Warren East, Chief

Executive |

warren.east@arm.com |

http://www.arm.com |

ARM.L

(FTSE250) |

21 Feb 2010 |

| Autonomy |

Mike Lynch, Chief

Executive |

mlynch@autonomy.com |

http://www.autonomy.com |

AU.L

(FTSE100) |

21 Feb 2010 |

| Leisure

&

Entertainment |

|

|

|

|

|

| Carnival (formerly P

and O) |

Micky Arison,

Chairman & Chief Executive |

marison@carnival.com |

|

CCL.L

(FTSE100) |

30 Jul 2010 |

| Football Association

(FA) Premier League |

Richard Scudamore,

Chief Executive |

rscudamore@premierleague.com |

|

|

21 Mar 2010 |

| Silverstone Circuits |

Richard Phillips,

Chief Executive |

richard.phillips@silverstone.co.uk |

|

|

21 Aug 2010 |

| Media |

|

|

|

|

|

| B Sky B |

Jeremy Darroch,

Chief Executive |

jeremy.darroch@bskyb.com |

http://www.bskyb.com |

BSY.L

(FTSE100) |

23 Oct 2009 |

| BBC |

Mark

Thompson, Director General |

mark.thompson@bbc.co.uk |

http://www.bbc.co.uk |

N/A |

15 Feb 2010 |

| BBC Today Program |

|

today@bbc.co.uk |

http://www.bbc.co.uk/today |

N/A |

5 Feb 2010 |

| BBC Watchdog |

|

watchdog@bbc.co.uk |

http://www.bbc.co.uk/watchdog/ |

N/A |

5 Feb 2010 |

| BBC Working Lunch |

|

workinglunch@bbc.co.uk |

http://www.bbc.co.uk/workinglunch/ |

N/A |

5 Feb 2010 |

| Channel 4 |

David Abraham, Chief

Executive |

dabraham@channel4.co.uk |

http://www.channel4.co.uk |

|

15 Jul 2010 |

| Daily Telegraph |

Will

Lewis, Editor |

will.lewis@telegraph.co.uk |

http://www.telegraph.co.uk

Tel: 0207 931 2000 |

N/A |

15 Feb 2010 |

| EMAP |

David Gilbertson,

Chief Executive |

david.gilbertson@emap.com |

http://www.emap.com |

Owned by Apax and

Guardian Media Group |

24 Nov 2009 |

| The Guardian |

Alan

Rusbridger, Editor |

alan.rusbridger@guardian.co.uk |

http://www.guardian.co.uk |

N/A |

5 Feb 2010 |

| The Independent |

Simon

Kelner, Editor |

s.kelner@independent.co.uk |

http://www.independent.co.uk

Tel: 020 7005 2000 |

N/A |

14 May 2010 |

| The Independent on

Sunday |

John Mullin, Editor |

j.mullin@independent.co.uk |

http://www.independent.co.uk |

N/A |

5 Feb 2010 |

| ITV |

Adam Crozier, Chief

Executive |

adam.crozier@itv.com |

http://www.itv.com |

|

21 May 2010 |

| PR Week |

Danny Rogers, Editor |

danny.rogers@haymarket.com |

http://www.prweek.com |

|

16 Sep 2010 |

| Reed Elsevier |

Erik Engstrom, Chief

Executive |

erik.engstrom@reedelsevier.com |

http://www.reedelsevier.com |

REL.L

(FTSE100) |

21 Feb 2010 |

| Reuters Group |

Tom Glocer, Chief

Executive |

tom.glocer@reuters.com |

http://www.reuters.com |

|

|

| The Sunday Times |

John Witherow,

Editor |

john.witherow@thetimes.co.uk |

http://www.timesonline.co.uk |

N/A |

5 Feb 2010 |

| The Times |

James Harding,

Editor |

james.harding@thetimes.co.uk |

http://www.timesonline.co.uk |

N/A |

5 Feb 2010 |

| YouView |

Roger Halton, Chief

Executive |

richard.halton@youview.com |

http://www.youview.com |

|

16 Sep 2010 |

| Metallurgy &

Minerals |

|

|

|

|

|

| Antofagasta |

|

|

|

ANTO.L

(FTSE100) |

|

| Anglo American |

Cynthia Carroll,

Chief Executive |

ccarroll@angloamerican.co.uk |

http://www.angloamerican.co.uk |

AAL.L

(FTSE100) |

5 Feb 2009 |

| BHP Billiton |

Marius Kloppers,

Chief Executive |

marius.kloppers@bhpbilliton.com |

http://www.bhpbilliton.com |

BLT.L

(FTSE100) |

21 Feb 2010 |

| Lonmin |

Ian Farmer, Chief

Executive |

ian.farmer@lonmin.com |

http://www.lonmin.com |

LMI.L

(FTSE100) |

9 Feb 2010 |

| Randgold Resources |

Mark Bristow, Chief

Executive |

mbristow@randgoldresources.com |

http://www.randgoldresources.com |

RRS.L

(FTSE100) |

21 Feb 2010 |

| Rexam |

Graham Chipchase,

Chief Executive |

graham.chipchase@rexam.com |

http://www.rexam.com |

REX.L

(FTSE100) |

21 Feb 2010 |

| Rio Tinto |

Tom Albanese |

tom.albanese@riotinto.com |

http://www.riotinto.com |

RIO.L

(FTSE100) |

21 Feb 2010 |

| Vedanta Resources |

MS Mehta, Chief

Executive |

ms.mehta@vedanta.co.in |

http://www.vedantaresources.com |

VED.L

(FTSE100) |

21 Feb 2010 |

| Xstrata |

Mick

Davis, Chief Executive |

mdavis@xstrata.com |

http://www.xstrata.com |

XTA.L

(FTSE100) |

8 Jan 2010 |

| Oil and Natural Gas |

|

|

|

|

|

| BG Group |

Frank Chapman, Chief